Discount

ASA's Discount to NAV

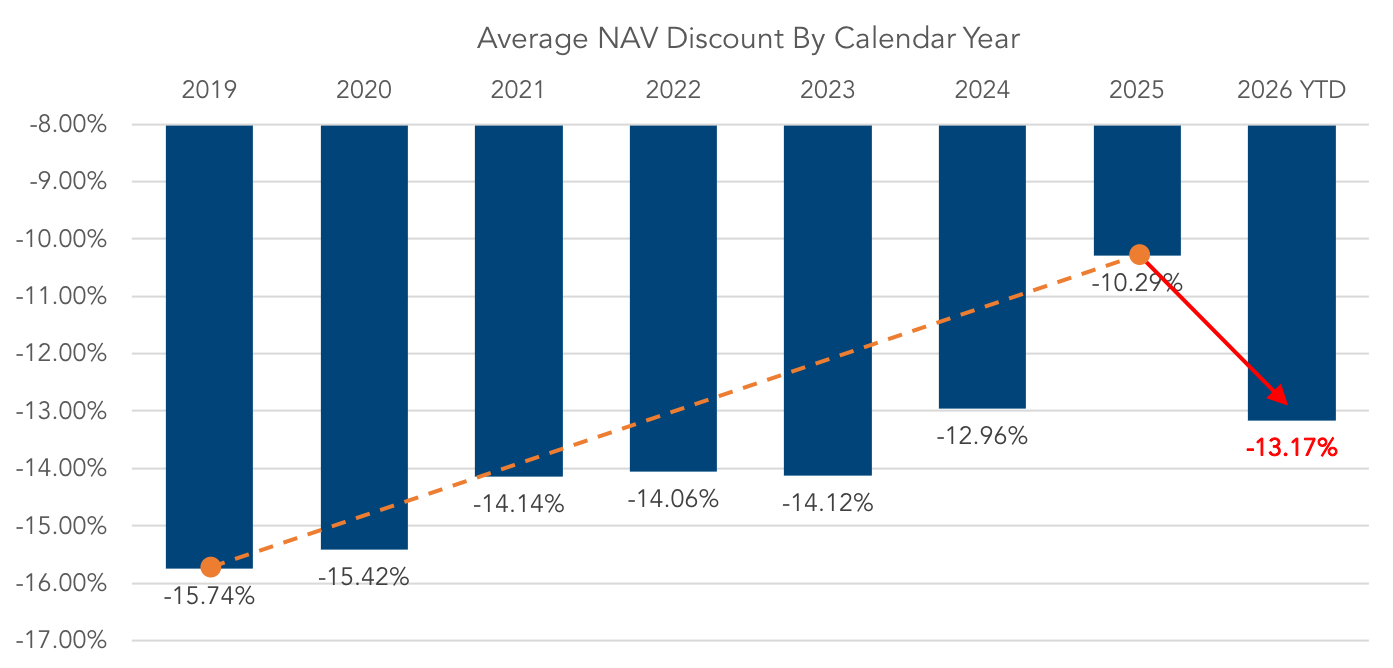

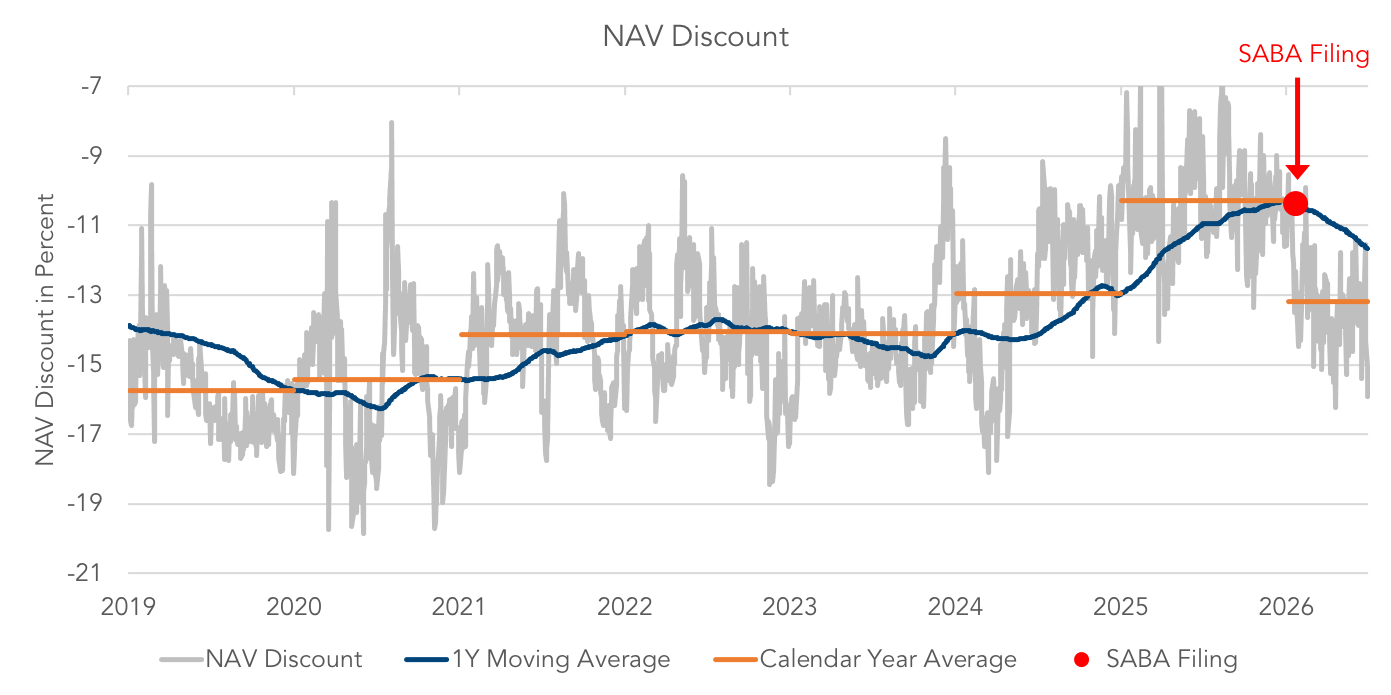

ASA’s discount narrowed after Merk began managing ASA in 2019. During Merk’s tenure, ASA delivered strong returns and helped restore investor confidence. That trend reversed sharply early this year after Saba disclosed plans to repurpose ASA away from its precious metals strategy.

Rather than narrowing the discount, Saba’s restructuring campaign has increased uncertainty around ASA’s future, created substantial and unnecessary tax consequences for shareholders, and may significantly delay any eventual tender offer or liquidity event.

ASA's discount narrowed despite significant uncertainty, including elevated expenses, turnover among corporate officers, and changes in key service providers in recent years.

An institutional shareholder holding approximately 12% of the Fund’s outstanding shares exited its position during the summer of 2025 amid developments at the Board level. Additional shareholders reduced or exited positions during this period of corporate uncertainty. These changes in the shareholder base occurred during a period of governance disruption, not investment underperformance.

The sustained narrowing of the discount during Merk’s tenure indicates that Merk’s initiatives had a measurable and consistent impact.

ASA’s Board received a proposal from Saba that proposed liquidation of the portfolio and restructuring of the Fund. Following the January 23, 2026, Schedule 13D filing, which outlined a potential shift away from ASA’s investment strategy, the discount widened to an average of 13.17% through June 30, 2026:

How the Discount Works—and Why It Matters

To assess recent developments, it is important to understand how ASA’s discount arises and how it has behaved over time.

ASA’s strategy justifies its closed-end structure—one that typically trades at a discount—by delivering strong long-term returns and access to investments not well suited for open-end funds.

- Only open-end vehicles can consistently trade at NAV.

- As open-end exchange traded products have a mechanism that fosters trading at or near NAV, the question becomes what the purpose of a closed-end fund is. Not only do closed-end funds not trade at NAV, they tend to have larger overhead than open-end funds because there are no multi-series umbrella type structures that provide cost efficiencies. In my assessment, a closed-end fund makes sense if it provides something that is not suitable for an open-end product, yet for which there is value to have it exchange traded for potential liquidity.

- This spirit was incorporated in ASA’s investment process under Merk, providing investors access to an approach well suited for a closed-end structure. This includes investing in smaller companies that are ill-suited for an exchange traded open-end product, yet may provide compelling sources of potential performance or a specific type of diversification and exposure. A side effect of investing in less liquid companies is that economic considerations suggest that a discount may arise when less liquid companies are accessible in a liquid wrapper. Such discount can be mitigated through a variety of measures; achieving long-term superior returns with this approach can more than compensate investors for the discount, as evidenced by ASA’s performance during Merk’s tenure managing the Fund. If coupled with carefully designed, periodic tender offers, these considerations may be balanced, providing the best of both worlds.

- Moving to more liquid securities may be appropriate during certain market environments based on the investment process but introduces the risk that the Fund looks more like an open-end product. If ASA’s strategy were shifted to fixed income, it raises the question whether the same strategy could be implemented in a lower-cost open-end structure.

- Unique to ASA is its status as a passive foreign investment company; amongst others, it adds additional overhead. The additional overhead is minor, as evidenced by ASA's low expense ratio when excluding extraordinary expenses. In a fixed income strategy, however, every basis point counts, and having overhead, even if only legacy overhead, may not be in the best interest of shareholders.

Saba’s Undisclosed Conflict

Neither Saba nor Paul Kazarian, a Saba partner and ASA director, has disclosed in Saba’s Schedule 13D or proxy filings that Saba hedges its precious metals exposure in ASA, even though Saba’s 13F filings reflect hedging activity. I believe that omission is material. Saba is seeking to dismantle ASA’s precious metals mandate while failing to disclose that it does not share the same economic interest as shareholders who invested in ASA for that mandate.

Path Forward

ASA’s discount narrowed during Merk’s tenure through disciplined management and shareholder-focused initiatives—and widened after Saba disclosed its intentions.

If governance is restored, ASA could re-emphasize the approach that delivered results under Merk:

- Reaffirm ASA’s precious metals strategy, which delivered strong performance under Merk

- Provide a structured exit for shareholders seeking liquidity

- Strengthen ASA’s investor base through renewed outreach and market engagement

Charts on this page as of June 30, 2026. Source: Bloomberg

Register your potential interest in a future Merk-managed mining strategy, so you don't miss out: saveasa.com/register

* The online registration is to indicate potential interest only. More information about a potential Merk-managed mining strategy will be provided at a later date. The past performance of ASA does not guarantee the future results of another Merk-managed strategy.

As of this writing, ASA’s Board has not announced how it will proceed. On June 30, 2026, Merk concluded its management of ASA after the Saba-controlled Board terminated Merk’s advisory agreement. Certain Fund directors, including a Saba partner, have assumed responsibility for ASA’s management.

Axel Merk owns over 300,000 shares of ASA Gold and Precious Metals Limited. He serves as President and Chief Investment Officer of Merk Investments LLC, which served as the Fund’s investment adviser until June 30, 2026. He also resigned as Chief Operating Officer of ASA in June 2026.

Nothing on this website constitutes an offer to sell, or a solicitation of an offer to buy, any securities. The information presented on this website reflects the views and opinions of Axel Merk and is provided solely for educational and informational purposes. It does not constitute investment, legal, financial, or tax advice. You should consult your own advisors for guidance specific to your circumstances.

The plans of Saba and the Board are based on publicly disclosed information only and are therefore accordingly qualified in their entirety and subject to change.

This site and its content have not been approved by ASA Gold & Precious Metals Ltd. (“ASA” or the “Fund”). concentrates its investments in the gold and precious minerals sector, which may be more volatile than other industries and influenced by changes in commodity prices driven by international economic and political developments. ASA is a non-diversified fund, which may result in higher risk through reduced portfolio diversification. It may also invest in smaller-sized and foreign companies, which may be more volatile, less liquid, and subject to additional risks, including currency fluctuations. Shares of closed-end funds like ASA frequently trade at a discount to net asset value.

This website may include forward-looking statements that reflect the current expectations, estimates, beliefs, assumptions, and projections of Axel Merk. These statements are inherently subject to risks and uncertainties, many of which are beyond the control of the author. Actual outcomes may differ materially from those discussed. Forward-looking statements can often be identified by words such as “believe,” “expect,” “intend,” “may,” “will,” “should,” or similar expressions including the negatives thereof, other variations or comparable terms. These statements speak only as of the date made, and there is no obligation to update or revise them in light of future developments.

Certain links may direct users to third-party websites or filings with the U.S. Securities and Exchange Commission (“SEC”). These materials are provided solely for convenience and informational purposes and are not incorporated by reference into any proxy materials. No responsibility is taken for the accuracy or content of third-party sources, and no obligation exists to provide updated information if it subsequently becomes incorrect in the future.